The energy prize on offer

In the United Kingdom, approximately one third of our CO2 emissions are produced running our homes. Useful reductions in home energy efficiency can be achieved at relatively low cost by simple measures such as blocking drafts and lagging boilers.

But moving towards carbon neutral homes requires major refurbishments such as installing triple glazing, modern boilers and solar powered water heating units.

Owner-occupiers need to have a high level of confidence in the long term (20 – 25 years) stability of house prices if they are to be persuaded to take out large loans to pay for expensive energy saving improvements. This confidence is currently lacking because after a long period when international house price inflation has exceeded general inflation, the banking crisis has produced a downturn in house prices.

How the system will work

We will refer to the British market but a similar system could be developed for other markets.

Background: How the Bank of England currently controls inflation

The Bank of England is responsible for setting the Bank Rate at a level which keeps national inflation within limits set by the government.

It has to use a single Bank Rate to cover the whole of the UK and all types of inflation.

So when a housing price bubble emerges in one part of the country, say the South East of England, it cannot be suppressed by increasing the Bank Rate without threatening the growth of whole of the UK economy

We propose the introduction of a Surcharge Interest Rate (SIR) which is only used to suppress excessive house price inflation. This rate can be fine tuned on a post code basis to meet local needs.

Making SIR politically acceptable

Mortgage payers would not lose the additional interest payments they make, but the money would be locked away in a savings account for up to twenty five years. To enforce this, anyone taking out a mortgage to purchase a property would also have to open a Bonded Savings Account.

Money could be paid into this account at any time but unless the account holder fell upon exceptionally hard times, money could not be withdrawn until the mortgage had been re-paid.

If house price inflation shows signs of outpacing general inflation, the Bank of England would have the power to impose a Surcharge Interest Rate on mortgages.

This SIR payment would be made into the Bonded Savings Account.

Effect on house prices

The payment of an effectively higher interest rate would take the heat out of the housing market, suppressing house price inflation.

In order to give the instrument bite, the SIR could be significantly (painfully) higher than the prevailing bank rate.

Minimising the financial burden for owner-occupiers

Owner-occupiers only bring the threat of inflation into the housing market at the time they are negotiating a price, so long standing mortgagees would not have to pay the current SIR.

The system would be backdated by (say) three months, to prevent speculative buying, in anticipation of a pending Surcharge Interest Rate rise. For example, if you take your mortgage out in October and the SIR increases in December, then you will have to make the SIR payments from December onwards.

Borrowing for Buy to let Affluent people who borrow money to buy properties for letting purposes do not contribute to the housing stock, but they add to the pressures on the housing market for as long as they possess a property. To partially redress this imbalance such borrowers would be subject to the current SIR throughout the life of their mortgage.

Focusing on housing inflation hot spots

The SIR could vary at post code levels because irrespective of where the mortgage is taken out, the location the property remains fixed. So, if you take your mortgage out in Bradford, but buy in London, you pay London SIR rates.

Once the local SIR had returned to a zero the cycle would start up again, with the most recent batch of SIR payers being freed from future payment obligations.

This local targeting of Surcharge Interest Rates would allow relatively large rates to be imposed without distorting the wider financial markets.

In part, the SIR mechanism is a psychological confidence building measure. Its presence will assure the markets that in the long term, house prices will keep in step with general inflation. This will reduce the benefits of speculative buying, consequently reducing the need for regular surcharge interest rate intervention.

SIR is not a substitute for building sufficient houses to meet house buyer demands, but it could support the house building programme.

The funds stored in the Bonded Savings Accounts could be hypothecated. That is, provide finance to support house building in areas where the demand for new homes was highest. In particular, the funds could be used to offset the additional costs commonly encountered when developing brown field sites. The Bank of England would have the final say on fund transfers, acting in the interest of the nation.

Bonded savings accounts for the super-rich

An alternative to Mansion Taxes

In central London especially, the super-rich help to create housing price bubbles because they are able to pay whatever house price the seller asks, without having to take out a mortgage loan.s

Butt their wealth and spending power creates jobs so we don’t want to drive them away by charging punitive council or mansion taxes. A variation on the bonded savings account theme would enable them to contribute in reducing the size of house price bubbles.

Anyone who buys a property for cash in a housing price bubble area should be required to open a bonded savings account and be obliged to pay in a sum proportionate to the price paid for the property each month. Their savings plus interest would be returned when they sold the property.

The accumulated funds would be made available for loans to developers wishing to build affordable homes in housing price bubble areas.

Long term benefits

Bonded savings accounts for the the super-rich would help to pull them into the country by keeping down the price of the most desirable properties.

Additional measures to stabilise house prices

We need reliable, reasonably priced public transport so that people can commute from areas of relative housing plenty to the big cities where available houses are scarce. For a solution to this problem please visit our Transport Internet page.

The inspiration for this proposal

The original version of this web page was published in June 2003 in response to a an article in the Economist magazine. This warned of a pending world wide crash in house prices.

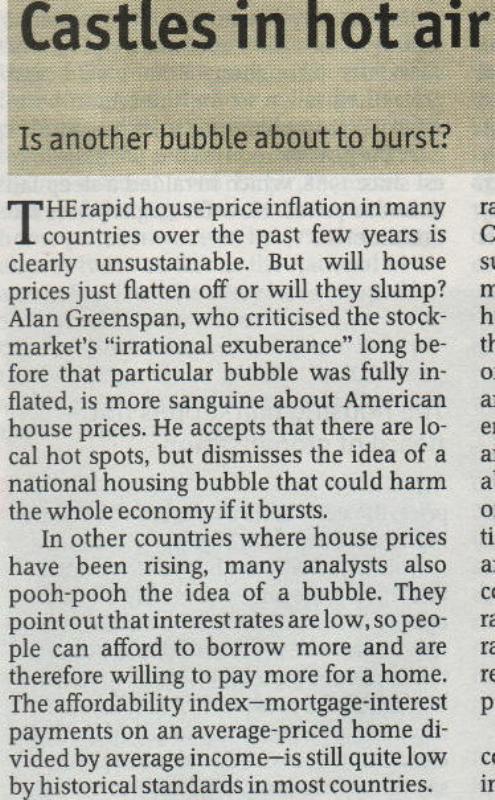

Figure 1. "Castles in hot air", Special supplement, The Economist, 31 May 2003.

History has shown that the Economist was right, with the collapse of the American sub prime housing market triggering a banking crisis and an international recession.

Here is a short extract from the 2003 Economist article

Figure 2. Bill Courtney disagreed with the Alan Greenspan analysis and tried to do something about it. But he was a virtually unknown aspiring inventor, so his lobbying of politicians and the financial media came to nothing.

Easing the Euro crisis

The SIR system would be particularly useful in large single currency territories such as the Euro and US dollar zones, because it would decouple local control of house price inflation from the bank rate set for the whole of the currency zone.

It's too late to solve the American sub-prime market problem but our proposal could boost confidence in Europe's ability to solve its current problems.

The menu of all inventions and innovations on this site is on the right.